Don’t Believe the Hype: ARMs Aren’t Taking Over the Mortgage Market

Let’s get something straight, fam: adjustable-rate mortgages (ARMs) aren’t suddenly dominating the U.S. housing market, no matter what shady tweets are floating through your feed 🧐. A recent viral post claimed a wild 41% of mortgages held by U.S. banks are ARMs, sending financial Twitter into a full-on meltdown. But spoiler alert: that number’s about as real as a rug-pull meme coin.

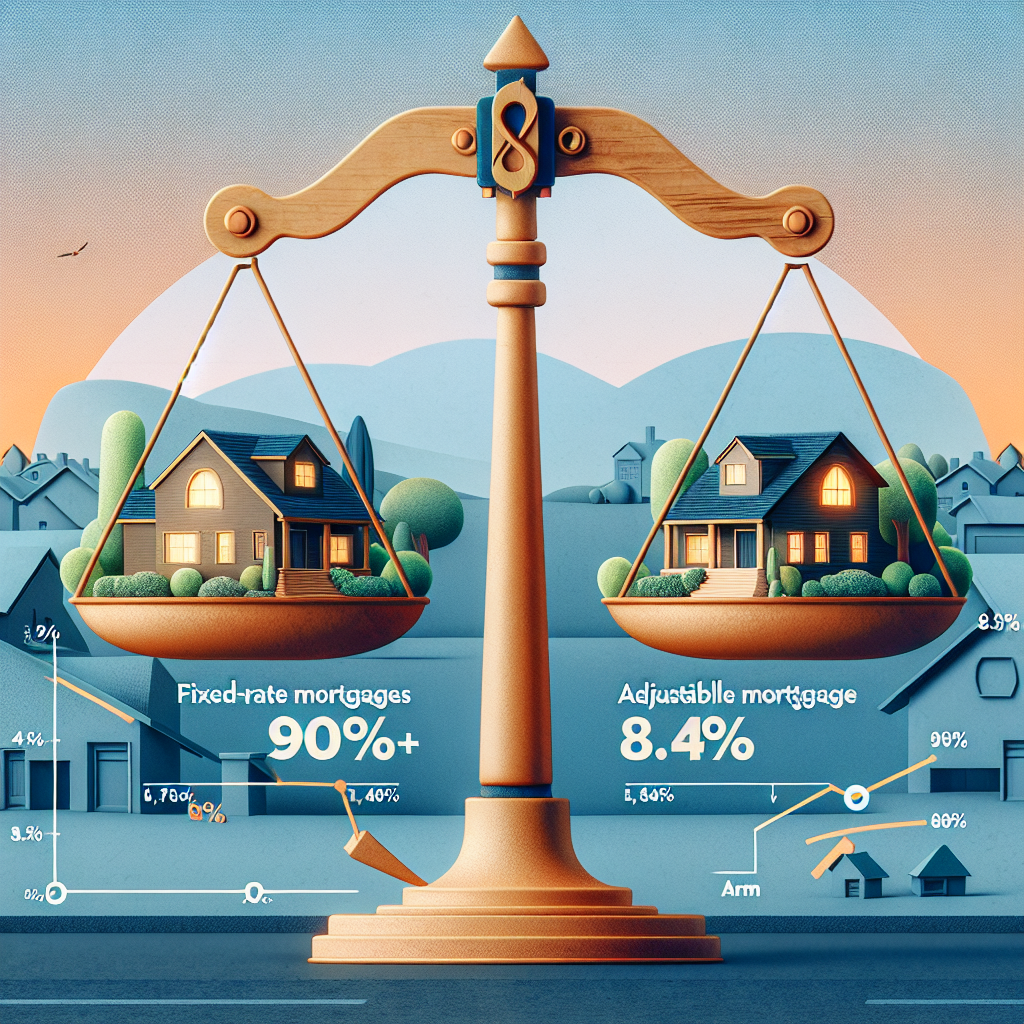

So what’s the truth behind the tweetstorm? According to HousingWire’s data-savvy mortgage maven Logan Mohtashami, there’s “no mathematical way” for 41% of American mortgages to be ARMs. The actual market share? Just 8.4% as of late August. Yep — not even hitting double digits. Mic drop 💁♀️.

ARMs: Still a Niche, But Not Dead

Now, let’s not toss ARMs completely into the history folder. They’ve been slowly crawling back into relevance, mostly because mortgage rates in general are giving 2000s energy — and not in a good way.

According to the Mortgage Bankers Association, ARM applications jumped 85% year-over-year recently. But math check 🧠: even that uptick only brought ARMs to 8.4% of total mortgage applications. Why the fuss, then? Well, the average ARM rate hovered at 6.19% while the popular (but pricey) fixed 30-year mortgage sat around 6.86%. You see the appeal, right?

But Wait… 41%? Where Did That Come From?

The viral drama may have started with a spicy tweet from Zero Hedge, claiming ARM loans made up 41% of U.S. bank mortgage holdings. That post spread faster than airdrop FOMO — but like many Web3 clickbaits, it left out a *critical* fine print: it likely referred to multifamily mortgages 👀. And not your average single-family, white-picket-fence dream home loans.

“Zero Hedge presents a consistently negative outlook — doom porn,” Mohtashami said in the HousingWire Daily podcast. 🔥 Tell us how you really feel, Logan! According to him, if you’re just looking at residential single-family homes — which is what most of us are dealing with IRL — ARM usage isn’t even close to tipping the scales.

This is all backed by receipts from the Federal Reserve Bank of St. Louis, which confirms that over 90% of U.S. mortgages are still good ol’ fixed-rate deals. Unlike places like Sweden and Canada, where ARMs run the show, America’s housing market has always had a soft spot for stability — and in today’s chaotic world, who can blame it?

New ARMs = Smarter, Safer

For the record, today’s ARMs aren’t the monster mashups of sketchy loans from the pre-2008 crash era. Forget those toxic, exotic structures that got a greenlight with zero due diligence back then. Now? Borrowers have to qualify for the *adjusted* rate, not just the tempting intro rate. That’s like Web3 token audits before the presale — more safety, less scammy.

So where’s this all going? Mohtashami suggests ARMs might inch up in market share if short-term rates keep drifting lower than their long-term counterparts. But don’t expect them to flip the game overnight. They’re more like that underrated altcoin in your wallet — could grow with the right market conditions, but not yet ready to moon 🚀.

TL;DR — Take the Hype with a Grain of Satoshi

In classic crypto-adjacent fashion, headlines move faster than facts, and virality doesn’t equal validity. ARMs may be trending, but they’re not taking over. So before you panic-sell your dreams of homeownership or prep for a 2008 replay, breathe easy. The fundamentals are still in check 💪.

Accuracy wins over alarmism 100% of the time — and that’s not just solid journalism, that’s alpha 🧠✨.

Until next time, keep questioning, keep learning, and always DYOR — even in the housing market 😉

– Anita