U.S. Treasury Proposes New Compliance Requirements for Payment Stablecoin Issuers

Here's what it means for you.

If you engage with payment stablecoins, new compliance requirements may affect transaction costs and operational transparency.

Why it matters

These regulations could reshape the landscape of digital finance, impacting how stablecoins operate and are perceived in the market.

What happened (in 30 seconds)

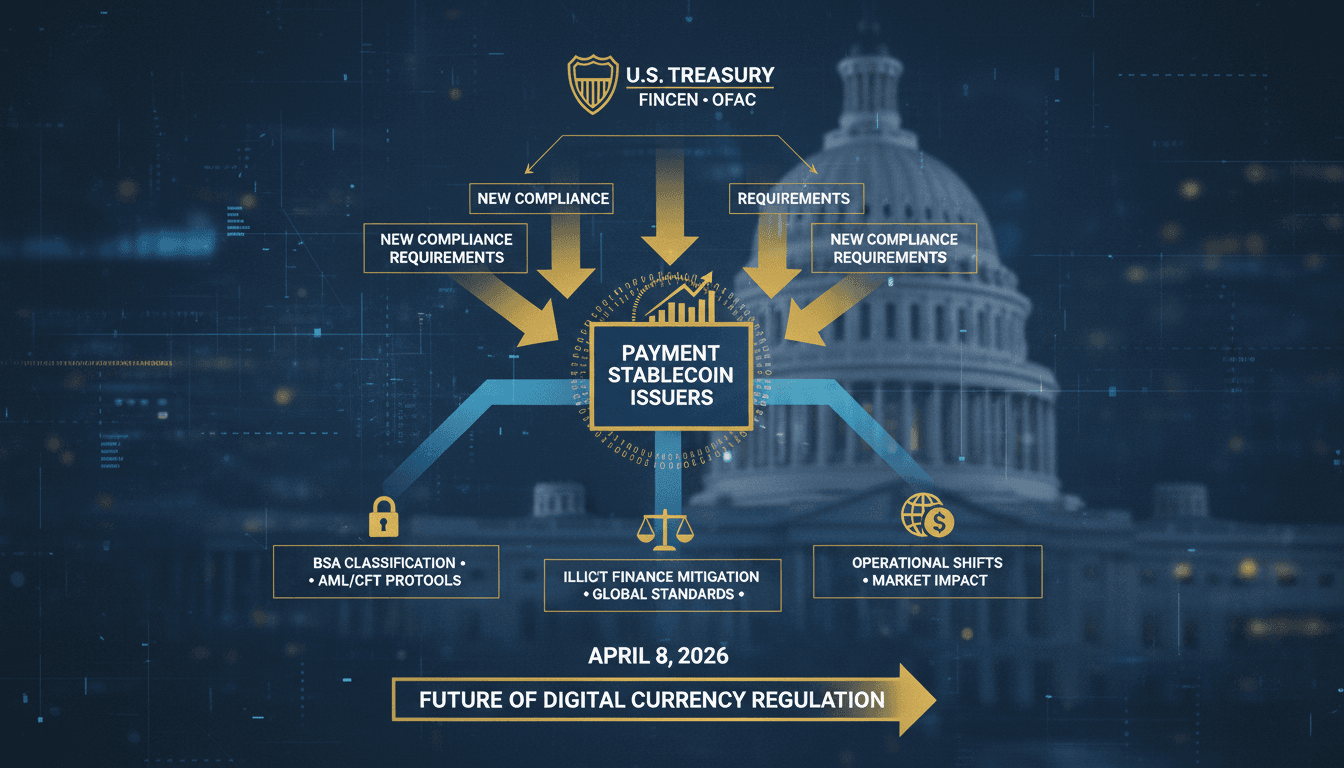

- On April 8, 2026, the U.S. Treasury proposed new compliance requirements for permitted payment stablecoin issuers, classifying them as financial institutions.

- The proposal mandates comprehensive anti-money laundering (AML) and countering the financing of terrorism (CFT) programs, along with sanctions compliance.

- Treasury Secretary Scott Bessent emphasized that these measures aim to protect the U.S. financial system while promoting innovation in digital finance.

The context you actually need

- The GENIUS Act, enacted in July 2025, established the first federal framework for payment stablecoins, limiting issuance to supervised entities.

- The total stablecoin supply reached approximately $316.8 billion as of early April 2026, indicating significant market growth and the need for regulatory oversight.

- Previous regulatory actions included proposals for reserve prudential standards and state oversight equivalence, indicating a broader trend towards stricter regulation of digital assets.

What's really happening

The U.S. Treasury's proposal represents a significant regulatory shift for the burgeoning stablecoin market, which has seen explosive growth and increasing scrutiny. By classifying permitted payment stablecoin issuers (PPSIs) as financial institutions under the Bank Secrecy Act, the Treasury aims to impose rigorous compliance requirements that align with traditional banking standards. This includes the establishment of board-approved AML/CFT programs, risk assessments, internal controls, independent audits, and the appointment of U.S.-based compliance officers.

The impetus for these regulations stems from concerns about the potential for stablecoins to facilitate illicit financial activities, especially as their market capitalization has ballooned. With the total stablecoin supply reaching $316.8 billion, the Treasury recognizes the need to mitigate risks associated with money laundering and terrorist financing. The proposed rules require issuers to file suspicious activity reports (SARs) for transactions exceeding $3,000, maintain comprehensive recordkeeping, and adhere to the Travel Rule for data transmission.

This regulatory framework is designed to balance the need for security with the promotion of innovation in digital finance. Treasury Secretary Scott Bessent has articulated that these measures are not merely punitive but are intended to foster a secure environment for digital financial technologies to thrive. The compliance burden will scale according to the size and risk profile of the issuer, which could lead to a consolidation in the market as smaller players may struggle to meet these new standards.

The implications of this proposal extend beyond U.S. borders, as international stablecoin issuers with operations in the U.S. will also need to comply. This could create a ripple effect, prompting other jurisdictions to adopt similar regulatory measures, thereby standardizing compliance requirements globally. As the market adapts to these changes, the focus will likely shift towards enhancing transparency and accountability in digital transactions.

Who feels it first (and how)

- Stablecoin Issuers: Companies like Circle and Tether will need to invest in compliance infrastructure, potentially increasing operational costs.

- Financial Institutions: Banks and financial services may face heightened scrutiny and collaboration with stablecoin issuers to ensure compliance.

- Consumers and Businesses: Users of stablecoins could experience changes in transaction fees and service availability as issuers adapt to new regulations.

What to watch next

- Public Comments: The upcoming 60-day public comment period will reveal industry sentiment and potential adjustments to the proposal.

- Market Reactions: Watch for responses from major stablecoin issuers and how they plan to adapt to the new compliance landscape.

- International Developments: Monitor regulatory actions in other countries that may align with or diverge from U.S. standards, affecting global stablecoin operations.

The U.S. Treasury has proposed new compliance requirements for stablecoin issuers.

Major stablecoin issuers will begin to adapt their operations to meet these new regulations.

The full impact on transaction costs and market dynamics remains to be seen as the industry responds.

Frequently Asked Questions

- Why it matters?

- These regulations could reshape the landscape of digital finance, impacting how stablecoins operate and are perceived in the market.

- What happened (in 30 seconds)?

- On April 8, 2026, the U.S. Treasury proposed new compliance requirements for permitted payment stablecoin issuers, classifying them as financial institutions. The proposal mandates comprehensive anti-money laundering (AML) and countering the financing of terrorism (CFT) programs, along with sanctions compliance. Treasury Secretary Scott Bessent emphasized that these measures aim to protect the U.S. financial system while promoting innovation in digital finance.

- What's really happening?

- The U.S. Treasury's proposal represents a significant regulatory shift for the burgeoning stablecoin market, which has seen explosive growth and increasing scrutiny. By classifying permitted payment stablecoin issuers (PPSIs) as financial institutions under the Bank Secrecy Act, the Treasury aims to impose rigorous compliance requirements that align with traditional banking standards. This includes the establishment of board-approved AML/CFT programs, risk assessments, internal controls, indepen

- Who feels it first (and how)?

- Stablecoin Issuers: Companies like Circle and Tether will need to invest in compliance infrastructure, potentially increasing operational costs. Financial Institutions: Banks and financial services may face heightened scrutiny and collaboration with stablecoin issuers to ensure compliance. Consumers and Businesses: Users of stablecoins could experience changes in transaction fees and service availability as issuers adapt to new regulations.

- What to watch next?

- Public Comments: The upcoming 60-day public comment period will reveal industry sentiment and potential adjustments to the proposal. Market Reactions: Watch for responses from major stablecoin issuers and how they plan to adapt to the new compliance landscape. International Developments: Monitor regulatory actions in other countries that may align with or diverge from U.S. standards, affecting global stablecoin operations.

Covers Bitcoin plus altcoin news, market updates, and educational resources.

"Bitcoin.com provides news, market data, and guides focused on Bitcoin and the wider crypto industry."

— A47 Editor

Treasury Proposes Stablecoin AML Rules as Bessent Vows to Protect US Financial System

The U.S. Department of the Treasury has proposed new anti-money laundering (AML) rules for stablecoin issuers, requiring them to monitor their own transactions to prevent illicit activities. This initiative, led by the Financial Crimes Enforcement Ne...

Real-time updates, analysis, and reports on the blockchain and cryptocurrency sectors.

"Crypto News delivers real-time updates, analysis, and reports on the blockchain and cryptocurrency sectors."

— A47 Editor

US Treasury plans sweeping AML leash for dollar stablecoin issuers

The US Treasury is set to implement comprehensive anti-money laundering (AML) and sanctions regulations for dollar stablecoin issuers, mandating the development of kill switches and robust compliance programs. This move aims to enhance oversight of o...