White House report reveals minimal impact of stablecoin yield prohibition on bank lending and consumer welfare

Here's what it means for you.

If you're a consumer or investor in the U.S. stablecoin market, the recent findings could affect your financial returns and banking options.

Why it matters

The prohibition on stablecoin yields is poised to reshape consumer welfare and bank lending dynamics in the U.S. economy.

What happened (in 30 seconds)

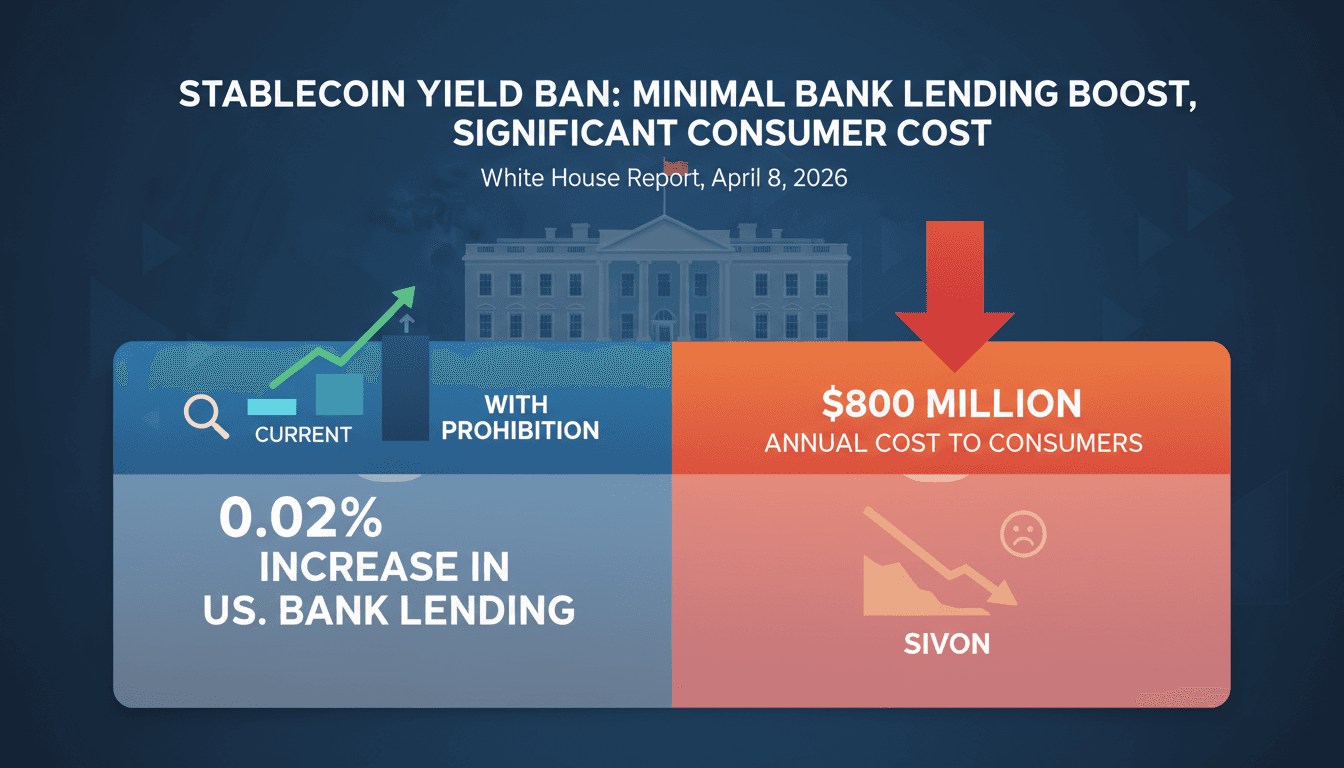

- On April 8, 2026, the White House Council of Economic Advisers published a report assessing the impact of prohibiting yields on stablecoins.

- The report concluded that this prohibition would only increase U.S. bank lending by 0.02% while imposing an $800 million annual net welfare cost on consumers.

- Concerns over deposit flight from banks to stablecoins were deemed quantitatively small, given the current liquidity in banks and the structure of stablecoin reserves.

The context you actually need

- The GENIUS Act, enacted in July 2025, established a regulatory framework for stablecoins, mandating reserves in safe assets and prohibiting direct yields.

- Stablecoins like USDC are primarily backed by Treasuries, with only a small percentage held in bank deposits, minimizing the risk of significant deposit flight.

- The CLARITY Act is currently being debated in Congress, aiming to extend yield prohibitions to intermediaries, amid lobbying from community banks concerned about stablecoin adoption.

What's really happening

The recent report from the White House Council of Economic Advisers sheds light on the ongoing debate surrounding stablecoin yields and their implications for the banking sector and consumer welfare. The findings indicate that the anticipated benefits of prohibiting yields on stablecoins—primarily aimed at safeguarding bank deposits—are significantly overstated. The projected increase in bank lending is a mere 0.02%, translating to approximately $2.1 billion in additional loans against a total U.S. loan book of $12 trillion. This marginal gain is overshadowed by the estimated $800 million annual cost to consumers, highlighting a substantial trade-off.

The GENIUS Act, which regulates stablecoins, was designed to mitigate risks associated with deposit shifts from traditional banks to yield-bearing stablecoins. However, the report reveals that stablecoins are predominantly backed by U.S. Treasuries rather than bank deposits, which means that the risk of deposit flight is minimal. For instance, Circle, a major stablecoin issuer, disclosed that only 12% of its USDC reserves are held in bank deposits. This raises questions about the necessity of stringent yield prohibitions, as the actual movement of funds from banks to stablecoins may not be as significant as previously feared.

Moreover, the introduction of products like Coinbase's USDC Rewards, which offers yield through revenue-sharing arrangements, complicates the regulatory landscape. While the GENIUS Act prohibits direct yields from stablecoin issuers, the ambiguity surrounding third-party yield-sharing has led to innovative financial products that could attract consumers. This dynamic creates a tension between regulatory intentions and market realities, as consumers seek higher returns in a low-interest-rate environment.

The implications for community banks are particularly pronounced. With over $1.1 trillion in excess reserves, banks are currently well-capitalized, but the fear of losing deposits to stablecoins remains a concern. The ongoing discussions surrounding the CLARITY Act, which aims to extend yield prohibitions to intermediaries, reflect the banking sector's apprehensions. However, the findings from the CEA report may shift the narrative, suggesting that the risks posed by stablecoins are manageable and that the focus should be on fostering a competitive financial landscape rather than imposing restrictive measures.

Who feels it first (and how)

- Consumers: Those invested in stablecoins may experience reduced returns due to yield prohibitions.

- Community Banks: Smaller banks concerned about deposit flight may feel pressure to adapt to changing consumer preferences.

- Stablecoin Issuers: Companies like Circle and Tether could face regulatory challenges that impact their business models.

What to watch next

- Senate Banking Committee deliberations: The outcome of the CLARITY Act negotiations will be crucial in determining the future of stablecoin regulations.

- Market response to stablecoin yields: Watch for shifts in consumer behavior and investment strategies in response to regulatory changes.

- Impact on community banks: Monitor how banks adapt to the evolving landscape and whether they implement new strategies to retain deposits.

The prohibition on stablecoin yields is expected to have a minimal impact on bank lending.

The CLARITY Act will continue to be debated, potentially leading to further regulatory adjustments.

The long-term effects on consumer welfare and banking practices remain to be seen.

Frequently Asked Questions

- Why it matters?

- The prohibition on stablecoin yields is poised to reshape consumer welfare and bank lending dynamics in the U.S. economy.

- What happened (in 30 seconds)?

- On April 8, 2026, the White House Council of Economic Advisers published a report assessing the impact of prohibiting yields on stablecoins. The report concluded that this prohibition would only increase U.S. bank lending by 0.02% while imposing an $800 million annual net welfare cost on consumers. Concerns over deposit flight from banks to stablecoins were deemed quantitatively small, given the current liquidity in banks and the structure of stablecoin reserves.

- What's really happening?

- The recent report from the White House Council of Economic Advisers sheds light on the ongoing debate surrounding stablecoin yields and their implications for the banking sector and consumer welfare. The findings indicate that the anticipated benefits of prohibiting yields on stablecoins—primarily aimed at safeguarding bank deposits—are significantly overstated. The projected increase in bank lending is a mere 0.02%, translating to approximately $2.1 billion in additional loans against a total U

- Who feels it first (and how)?

- Consumers: Those invested in stablecoins may experience reduced returns due to yield prohibitions. Community Banks: Smaller banks concerned about deposit flight may feel pressure to adapt to changing consumer preferences. Stablecoin Issuers: Companies like Circle and Tether could face regulatory challenges that impact their business models.

- What to watch next?

- Senate Banking Committee deliberations: The outcome of the CLARITY Act negotiations will be crucial in determining the future of stablecoin regulations. Market response to stablecoin yields: Watch for shifts in consumer behavior and investment strategies in response to regulatory changes. Impact on community banks: Monitor how banks adapt to the evolving landscape and whether they implement new strategies to retain deposits.

News, analysis, and thought leadership focusing exclusively on Bitcoin.

"Bitcoin Magazine is one of the original publications devoted to Bitcoin, offering in-depth news, analysis, and commentary."

— A47 Editor

White House Says Banning Stablecoin Yield Would Hurt Consumers More Than It Helps Banks

A White House economic analysis indicates that banning stablecoin yield would result in minimal benefits for bank lending while significantly impacting consumers by reducing their returns. This assessment highlights the potential drawbacks of restric...

Covers blockchain, cryptocurrency news, project analysis, and market insights.

"CoinDesk is a well-established cryptocurrency and blockchain news provider, offering comprehensive insights, market data, and industry research."

— A47 Editor

White House study bolsters crypto's stance in stablecoin yield fight against bankers

A recent White House study indicates that banning rewards from stablecoins would not significantly enhance the financial health of banks, reinforcing the crypto industry's position in ongoing discussions surrounding the Clarity Act.