Moody's Revises U.S. Business Development Companies Outlook to Negative

Here's what it means for you.

If you're involved in private credit investments, this shift could signal increased risk and volatility in your portfolio.

Why it matters

This revision indicates potential instability in the private credit market, which could affect funding access for middle-market companies.

What happened (in 30 seconds)

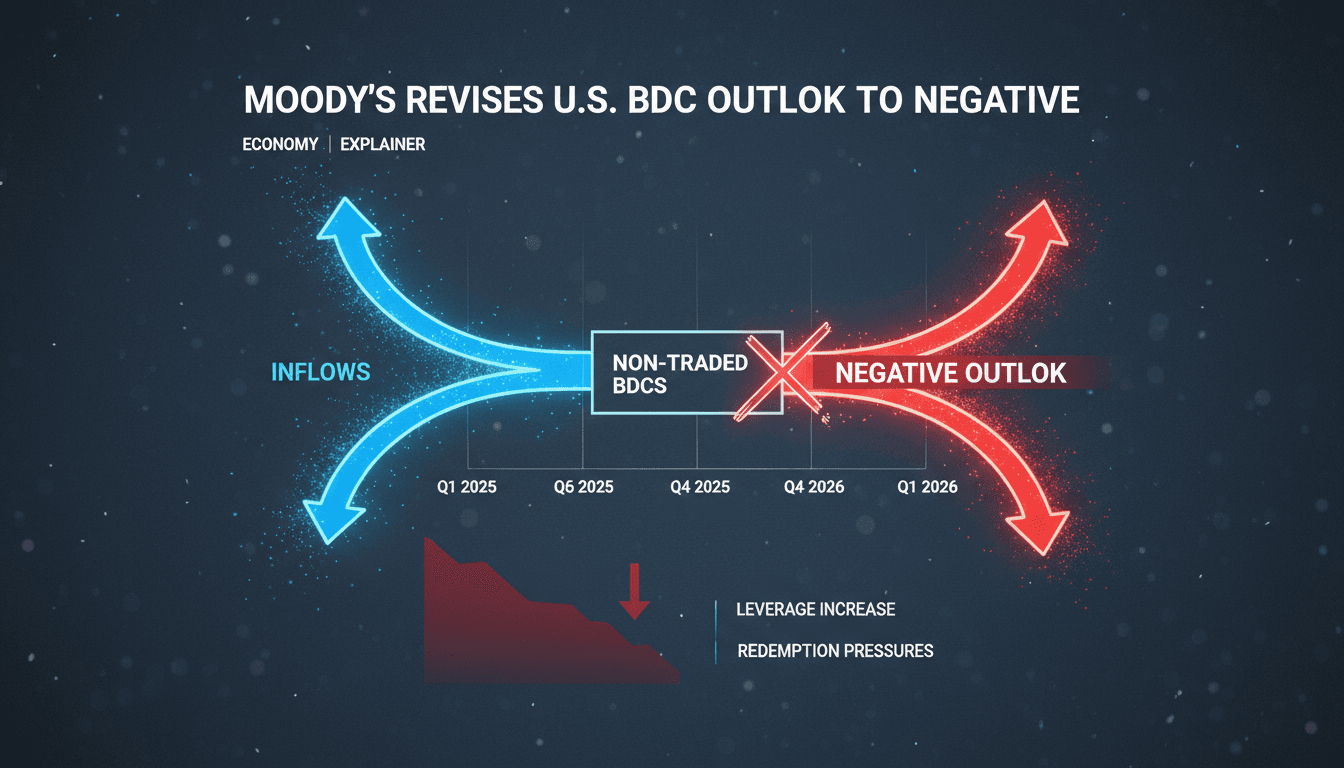

- Moody’s Ratings revised its outlook for U.S. business development companies (BDCs) from stable to negative on April 7, 2026.

- Non-traded BDCs, which make up over 60% of the sector, faced unprecedented outflows and increased leverage pressures.

- Access to funding markets weakened as bond spreads widened, raising concerns about credit performance amid economic uncertainty.

The context you actually need

- Business development companies (BDCs) are regulated investment firms that provide financing to middle-market companies, similar to private credit funds.

- Non-traded BDCs dominate the sector, having previously enjoyed robust inflows in Q3 2025, but early 2026 marked the first outflows due to rising economic pressures.

- Portfolio risks are heightened by a significant exposure to technology sectors, particularly software firms, which are vulnerable to AI-driven disruptions.

What's really happening

On April 7, 2026, Moody’s Ratings announced a significant shift in its outlook for U.S. business development companies (BDCs), moving from a stable to a negative assessment. This change is primarily driven by rising redemption pressures in non-traded BDCs, which represent more than 60% of the sector. These companies have experienced their first-ever outflows in early 2026, a stark contrast to the robust inflows seen in the third quarter of 2025. This reversal is indicative of growing investor concerns amid a backdrop of economic uncertainty, including higher interest rates and portfolio risks.

The increased leverage among BDCs has further complicated the situation. Typically, BDCs operate with a debt-to-equity ratio of around 1:1, but many are now exceeding this limit, which strains their access to funding. As bond spreads widen, BDCs are retreating from unsecured bond markets, limiting their ability to secure necessary capital. This tightening of funding access is expected to weaken credit performance across the sector.

Moreover, the exposure of BDC portfolios to technology firms, particularly those in the software sector, raises additional risks. With approximately 25% of BDC investments tied to companies susceptible to AI-driven technological disruption, the potential for significant losses looms large. Moody’s anticipates that these factors will position BDCs as an early indicator of stress within the private credit sector, suggesting that broader implications for the market may be on the horizon.

The revision of the outlook serves as a warning signal not only for BDCs but also for investors and stakeholders in the private credit landscape. As liquidity and asset quality come under scrutiny, the potential for declines in BDC stock prices could create ripple effects throughout the financial ecosystem.

Who feels it first (and how)

- Investors in BDCs: Those holding shares in non-traded BDCs may face immediate financial implications due to potential declines in stock value.

- Middle-market companies: Businesses relying on BDC financing could experience tighter funding conditions, impacting their growth and operational strategies.

- Financial analysts and advisors: Professionals monitoring private credit markets will need to reassess risk profiles and investment strategies in light of the revised outlook.

What to watch next

- Redemption trends: Continued outflows from non-traded BDCs will be critical to monitor, as they could signal deeper liquidity issues.

- Interest rate movements: Changes in interest rates will affect borrowing costs and access to capital for BDCs, influencing their operational viability.

- Technological disruptions: The impact of AI on portfolio companies, particularly in the tech sector, will be essential to assess for potential credit risks.

The outlook for U.S. BDCs has been revised to negative, indicating heightened risk.

Continued scrutiny of BDC liquidity and asset quality will emerge as investors react to the revised outlook.

The full extent of the impact on middle-market companies and the broader private credit market remains uncertain.

Frequently Asked Questions

- Why it matters?

- This revision indicates potential instability in the private credit market, which could affect funding access for middle-market companies.

- What happened (in 30 seconds)?

- Moody’s Ratings revised its outlook for U.S. business development companies (BDCs) from stable to negative on April 7, 2026. Non-traded BDCs, which make up over 60% of the sector, faced unprecedented outflows and increased leverage pressures. Access to funding markets weakened as bond spreads widened, raising concerns about credit performance amid economic uncertainty.

- What's really happening?

- On April 7, 2026, Moody’s Ratings announced a significant shift in its outlook for U.S. business development companies (BDCs), moving from a stable to a negative assessment. This change is primarily driven by rising redemption pressures in non-traded BDCs, which represent more than 60% of the sector. These companies have experienced their first-ever outflows in early 2026, a stark contrast to the robust inflows seen in the third quarter of 2025. This reversal is indicative of growing investor co

- Who feels it first (and how)?

- Investors in BDCs: Those holding shares in non-traded BDCs may face immediate financial implications due to potential declines in stock value. Middle-market companies: Businesses relying on BDC financing could experience tighter funding conditions, impacting their growth and operational strategies. Financial analysts and advisors: Professionals monitoring private credit markets will need to reassess risk profiles and investment strategies in light of the revised outlook.

- What to watch next?

- Redemption trends: Continued outflows from non-traded BDCs will be critical to monitor, as they could signal deeper liquidity issues. Interest rate movements: Changes in interest rates will affect borrowing costs and access to capital for BDCs, influencing their operational viability. Technological disruptions: The impact of AI on portfolio companies, particularly in the tech sector, will be essential to assess for potential credit risks.

Market-moving headlines impacting equities, bonds, and related risk assets.

"Real-time catalysts and volatility drivers across indices and sectors."

— A47 Editor

Moody’s cuts outlook on US BDCs to ’negative’ on redemption pressure, rising leverage

Moody's has downgraded its outlook on U.S. Business Development Companies (BDCs) to negative, citing increased redemption pressures and rising leverage within the sector. This decision reflects growing concerns about the stability of private credit m...

Global markets, investing, and macroeconomics from a premier financial newsroom.

"Bloomberg is respected for in-depth financial reporting and data-driven analysis."

— A47 Editor

Private Credit Exodus Turns Moody’s Outlook on BDCs to Negative

Moody's Ratings has revised its outlook for private credit investment vehicles to negative, following a significant increase in redemptions that has disrupted the market after a stable period of over two years.